Visa Europe revealed important stats about the usage of Contactless Cards. Poland, Spain and the UK use this payment methd the most, with UK usage growing by 300% year over year.

.png)

David E. Acosta April 8, 2022

📣 Big announcement: we have now been listed on the SWIFT Customer Security Programme (CSP) Assessment Providers directory.

Contact us now to validate your compliance posture with SWIFT CSP requirements:

The exchange of goods has always been present in the history of mankind and is a fundamental part of the economy. With the arrival of banks and savings banks as custodians of assets, the need to guarantee the safe movement of money between accounts arose. Initially, these financial movements were recorded manually, resulting in delays, transcription errors, and fraud.

With the advent of telegraph-based telecommunications, the time associated with the processing of this type of transaction (called "Telegraphic Transfers" or TT), typically took between two and three business days to be processed, especially in asset transfers between financial institutions located in different parts of the world (international transfers), was optimized. These times in interbank operations were minimized with the evolution of telecommunications networks, without the need to physically exchange money and using only electronic records, a process called "electronic funds transfer" or EFT.

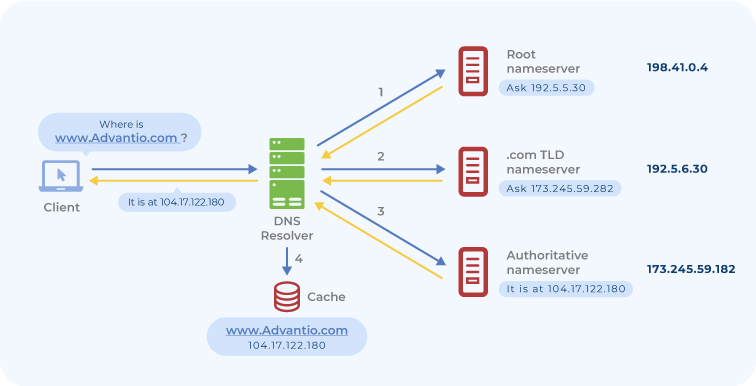

Initially, interbank transfers were managed directly between the two entities involved in the transaction (sender and receiver). However, given the number of banking entities in the world, the management of one-to-one transactions became a titanic task, whose only solution was the use of an intermediary entity acting as a concentrator or "hub" for the routing of transfers.

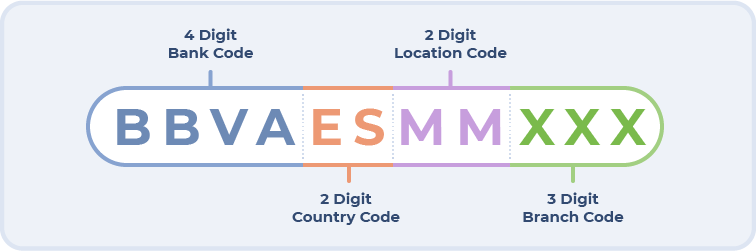

In response to this need, the Society for Worldwide Interbank Financial Telecommunication (SWIFT) was founded in 1973 in Belgium, a cooperative entity composed at that time of 240 banks in 15 different countries, whose objective was to serve as an intermediary for the execution of financial transfers between banking entities. SWIFT offers not only services related to financial transfers, but also a communications and software infrastructure that facilitates the routing of transactions (or "messages") and the identification of the different entities involved in the transaction, where an alphanumeric system is used to identify each member organization, indistinctly referred to as "bank identifier code" (BIC), SWIFT code, SWIFT ID, or ISO 9362 code.

As with any service of this type, not only interoperability and response, times are important, but also security. The SWIFT messaging system requires high levels of protection against unauthorized modification, availability, confidentiality, and the ability to track activities (traceability), since the trust of customers is built on these features. As a result, the SWIFT system was attacked in 2015 (TPBank in Vietnam and Banco del Austro in Ecuador) and 2016 (Akbank in Turkey and Central Bank of Bangladesh), causing millions of dollars in losses and forcing SWIFT to take detective and corrective measures to minimize the impact of future attacks.

SWIFT Customer Security Controls Framework (CSCF) and Customer Security Programme (CSP)

Due to the attacks on SWIFT's infrastructure, the SWIFT Customer Security Controls Framework (CSCF) was published in 2017, which outlines a series of measures designed to protect the SWIFT network infrastructure. These controls are updated annually to align protection levels with the evolution of both attack techniques and underlying technology:

These controls are divided into two categories:

The relevant SWIFT CSCF 2024 controls are organized into three main objectives, supported by seven principles and 32 controls, 25 of which are mandatory and 7 of which are recommended:

1. Secure your environment:

2. Know and limit Access:

3. Detect and respond:

As a complement to the security controls themselves, SWIFT CSCP also includes a descriptive guide for the identification of services and components within the scope of compliance (including production processing, backup, and disaster recovery locations), different types of component deployment architecture to validate the applicability of controls and assets, a list of risks and their corresponding mapping with their countermeasure, an inventory of example threat scenarios, a table identifying the relationship of SWIFT's control objectives with the requirements of the NIST Cybersecurity Framework, ISO/IEC 27002 and PCI DSS, and a table of shared responsibilities when using services from external providers (including cloud service providers - CSPs).

SWIFT CSCF controls, in conjunction with other documents such as SWIFT Customer Security Controls Policy (CSCP) and SWIFT Information Sharing and Analysis Centre (ISAC), are managed through the SWIFT Customer Security Programme (CSP), which describes the processes for compliance reporting, third party security status verification and follow-up remediation actions for non-compliance.

Implementation and compliance plan

For entities facing the SWIFT CSCF controls deployment process for the first time or organizations that already have some level of cybersecurity maturity, defining an interactive methodology that facilitates the security controls lifecycle will optimize the time and effort in securing the local SWIFT services infrastructure.

In this sense, the recommendation is to proceed in a similar way to that followed in the implementation of other standards: by using the Deming cycle or Plan-Do-Check-Act (PDCA):

The monitoring and support of a specialized entity in each of these phases is advisable, as it will ensure that the strategic objectives defined and the associated tactical actions are aligned with the criteria defined by SWIFT CSP, which will minimize the occurrence of unforeseen tasks during the course of the cycle over time, thus defocusing the previously defined efforts.

Compliance evaluation and reporting process

In order to validate that an organization connected to the SWIFT infrastructure complies with the security controls described in SWIFT CSCP, the compliance status of these controls must be reported based on the SWIFT CSP guidelines, which specify that all customers must report their compliance posture using the Know Your Customer (KYC) tool on an annual basis or when there is a change in scope. As of July 2021, this compliance assessment is required to be performed independently without interference from the business units. For this, there are two alternatives:

The compliance report should indicate whether the entity is compliant with the SWIFT CSCF control objectives, will be compliant in the future (which implies an action plan), is not compliant or the control is not applicable. This report will be visible to both SWIFT and the counterparties (financial institutions).

As a result of the SWIFT CSP transparency criteria, if an organization fails to adhere to the SWIFT CSCF controls, other members of the SWIFT community may have access to this information (which will affect relationships with third parties) or the affected entity may be disconnected from the SWIFT network.

How can Advantio help in this process?

Based on Advantio's expertise in payments and cyber security, we offer the following services for implementation and independent assessment of compliance with SWIFT CSCF controls in accordance with SWIFT CSP:

I am the Senior Security Consultant in Advantio. I have more than 15 years of experience, working both in South America and Europe. My information security background includes consultancy and audit, training, implementation of security technologies and design and policy development among others.

Certifications: CISSP, CISM, CISA, CRISC, CEH, CHFI, PCI QSA, QSA (P2PE), 3DS Assessor

Comments